UK's most recent gambling industry statistics

Published on September 2, 2017, 8:27 am

by Jeff Grant ![]()

The growing diversity of gambling opportunities available in the UK is undoubtedly posing challenges to the land-based casino industry. The rapid growth in the accessibility of online casinos and the increasing variety offered by online sports books are just two of the reasons as to why UK casinos seem to be in a state of stagnation when compared to their rivals.

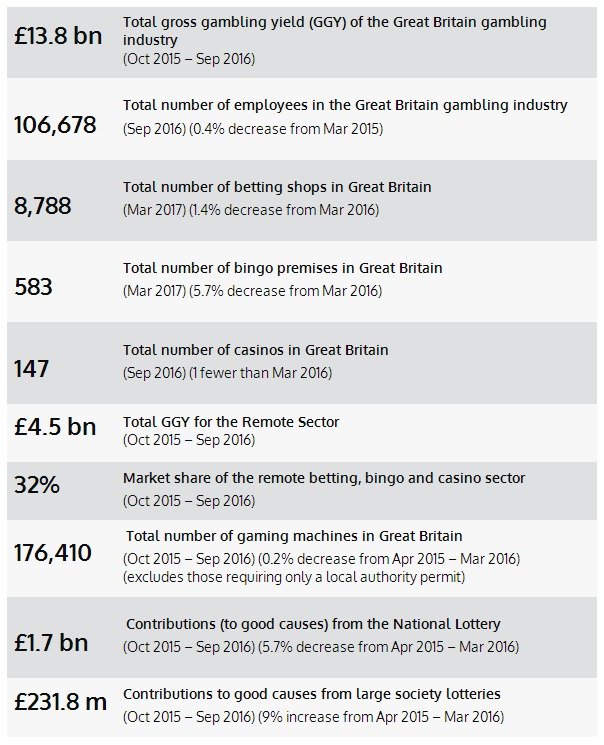

The most recent industry statistics released by the UK Gambling Commission (covering the period October 2015 - September 2016) show that at 147, the number of land-based casinos in the UK is actually lower than it was in March 2016, and that the much-anticipated growth in the industry via the introduction of ‘super casinos’ across the country has not materialised, with only four of the eight proposed sites currently operating.

This stagnation in the UK casino industry (which could in reality be viewed as a decline) is further borne out by the figures in the UKGC Industry Statistics report, which show that the gross gambling yield (GGY) of UK casinos for the period was £1.189 billion, a very modest increase of just over £30 million from the previous report (April 2014 - March 2015), and which represents just 9% of the entire UK GGY.

In comparison online gambling, with a GGY of £4.5 billion, now makes up 32% of the entire yield for the UK, of which online casino games (largely slots games) contribute £1.6 billion, almost half a billion pounds more than is being wagered in land-based casinos.

And while newer forms of online gambling are presenting the casino industry with stiff competition, there is also the sense that land-based casinos are not responding with any great imagination or innovation, particularly when compared to other similar markets elsewhere around the world.

For instance, the latest statistics from the US show that in 2015 gross gaming revenue generated by land-based casinos was USD$38.54 billion, a record high and a 2.2% increase on the 2014 figures. 17 of 24 states that operate casinos (71%) saw an increase in revenue from 2014, with new casinos opening in Maryland, Ohio and Louisiana.

New Zealand too showed a significant increase in the revenue generated by casinos, at NZD$586 million in 2015/16 up from NZD$527 million in 2014/15, representing an increase of around 11%. In Australia, there has also been significant growth in casino turnover, up 11.9% to AUD$1.375 billion in 2014/15 (the last year that full data is available) from the previous year.

So what can UK land-based casinos do, and what lessons can they learn from overseas rivals?

Admittedly, casinos in Australia and New Zealand benefit from their closer proximity to Asia and so in terms of travel times they are instantly more appealing to Chinese high rollers, but UK casino operators could nevertheless take a leaf out of their books in terms of the facilities and games they offer Asian punters.

For instance, there is currently about AUD$10 billion worth of casino development projects in the pipeline in Australia in popular tourist destinations like the Gold Coast, much of which will be centred around attracting big-spending Chinese gamblers. As much luxury resort as casino, they include five- and six-star hotels, theatres and entertainment, beach clubs and other facilities designed to attract those with money to burn and who want more than simply being comped a hotel room.

As further evidence of the Australian casino building boom, Crown Resorts plans to build a AUD$2 billion casino and six-star hotel on Sydney Harbour, Star Entertainment has plans in place to build a AUD$3 billion casino resort in Brisbane, while SkyCity has recently commenced a AUD$330 million expansion of its casino in Adelaide. All of these projects are designed to attract not only high rollers but premium tourists by offering more than just a gaming floor.

UK casinos also tend to fall short when it comes to offering other forms of entertainment besides gambling. The show biz scene in Las Vegas is of course legendary, but other US and Canadian casinos also work harder than their UK counterparts at making entertainment one of their prime attractions.

For example, the newest venue in the UK, The Victoria Gate Casino in Leeds city centre, has a pretty low-key entertainment schedule when compared to even a relatively small regional casino in North America, featuring predominantly local rather than big-name or international acts. UK casinos need to work harder to shift the public perception of what a casino can offer by broadening the scope and upping the quality of the entertainment they provide, and seek to make it a major draw in and of itself rather than just a sideline, or background music to the hum of the slots.

UK casinos could also perhaps look at having increased sports betting facilities onsite. While the new Victoria Gate Casino in Leeds does have a bar dedicated to sports and where you can bet on local and international events via live betting terminals, sports betting is not a feature at the majority of UK casinos, and with online sports betting producing a GGY of £1.9 billion in 2015/16, this is an area that land-based casinos could further exploit, not only in terms of increasing participation but also in appealing to a broader demographic.

It can also be argued that the whole approach to the marketing of land-based casinos is not sufficiently appealing to the 18-40 age group, especially when compared to how online sports books and casinos capture their audiences. Online and mobile casinos, for instance, are moving more into the areas of personalising the punter’s experience, with special offers and promotions tailored to the individual player. Many UK online casino brands are certainly ahead of their land-based rivals when it comes to offering players an interactive, personalised gaming experience, and this is therefore another area where UK bricks and mortar venues need to catch up.

Perhaps part of the image problem facing UK casinos also comes from the public furore surrounding fixed odds betting terminals (FOBTs) which are available in high street bookmakers. There is much debate over these machines, with calls for bet limits and in some cases outright bans. While you can’t play FOBTs in casinos, it can be argued that public mistrust directed towards this highly visible form of gambling has meant that casinos have inadvertently been affected, and that they haven’t done enough to counter this image problem.

There also needs to be some strategic, out-of-the-box thinking in terms of providing customers with what they want from a casino and entertainment facility. While the thought of it might be anathema to some, in the US there are growing numbers of casinos that offer childcare facilities to players. If UK casinos are going to compete against their online rivals, then they need to find ways to entice punters away from their screens and onto the gambling floor, and so such a radical innovation could be one of a range of solutions to arrest declining patronage.

Overall, therefore, it can be seen that UK land-based casinos face some very significant challenges in terms of the quality of their facilities, the range of entertainment they offer, and the way they market themselves to a younger generation of punters, and need to respond positively if they are going to stand up to the increasingly stiff competition being offered by their online rivals.

COMMENTS:

By loading and joining the Disqus comments service below, you agree to their privacy policy.